Wealth

Warren Buffett’s Simple Guide to Getting Started in Investing

- 02 Mar 2026

Learn how to apply for student grants step by step, from gathering documents and completing financial aid forms to finding extra opportunities and meeting deadlines. This guide explains how to maximize your chances of getting free money for school this year....

Women and minority entrepreneurs have more funding options than ever, including SBA-style loans, community lenders, banks, microloans, and online financing. This guide explains where to find capital, how to qualify, and how to choose the right loan to grow your business....

Learn what to do after a car accident to get the most from your insurance, including documenting the scene, understanding your coverage, handling repairs and medical claims, and avoiding common mistakes that can cost you money or delay your payout....

Telehealth and digital care are transforming health insurance by lowering costs, expanding access, and improving convenience. This guide explains how virtual care works, what plans now cover, and how using digital health services can help you save money and get faster, easier care....

Learn what cryptocurrency is, how blockchain works, the main types of crypto assets, key risks, and smart beginner strategies. This guide explains what to know before investing in crypto so you can avoid common mistakes and invest more responsibly....

Learn who you can legally claim as a dependent, including children, relatives, and special cases like shared custody or multiple support situations. This guide explains the rules, common mistakes, and how to claim dependents correctly to avoid problems and maximize tax benefits....

Taxes are withheld from paychecks as estimated payments toward annual obligations. After filing a return, total income, deductions, and credits determine the actual amount owed. Overpayments result in refunds, while underpayments require paying the remaining balance....

Understand how taxes really work, from income and tax brackets to deductions, credits, and refunds. This simple guide explains what you pay, why you pay it, and how to legally reduce your tax bill with smarter planning....

This guide explores the best side hustles for 2026, from digital products and freelancing to e-commerce and content creation, and explains how to choose scalable income streams that build long-term wealth instead of just short-term extra cash....

Learn how the tax system works in simple terms, including income, tax brackets, deductions, credits, and refunds. This guide explains what you owe, why you owe it, and how to manage taxes smarter and with less stress....

This beginner’s guide explains how cryptocurrency works, why people are moving from cash to digital assets, and how to use crypto responsibly as part of a diversified wealth-building strategy while understanding the risks and opportunities....

A debt payoff playbook helps you track balances, choose a smart strategy, and stay consistent. By planning, automating payments, and monitoring progress, you can eliminate debt faster, stay motivated, and build lasting financial control....

Cryptocurrency is reshaping how people build wealth by introducing a new digital asset class. Learn how crypto works, why it matters, its risks, and how to use it wisely as part of a smart, diversified investment strategy....

A debt payoff planner gives you a clear, step-by-step blueprint to eliminate debt faster, reduce interest, and stay motivated. By organizing balances, choosing the right strategy, and tracking progress, you can take control of your finances and build a lasting debt-free future....

Using a loan responsibly means borrowing for the right reasons, only what you can afford, understanding the true cost, and having a clear repayment plan. Smart borrowing protects your finances and credit, while careless use can lead to long-term debt and stress....

Short-term and emergency loans offer fast cash in urgent situations but come with high costs and serious risks. Used carefully and only for true emergencies, they can help bridge gaps, but repeated use or poor planning can lead to debt traps and long-term financial trouble....

Your credit score determines which loans you can access and how much interest you pay. Higher scores unlock better rates and more options, while lower scores mean fewer choices and higher costs. Improving your score can significantly reduce borrowing expenses....

Debt consolidation can simplify multiple payments into one and lower interest costs when you qualify for a better rate and commit to avoiding new debt. Used wisely, it can create a clearer, more affordable path toward becoming debt-free....

Your credit score is built from payment history, credit utilization, account age, credit mix, and new credit activity. Paying on time, keeping balances low, and avoiding too many applications are the most effective ways to improve and maintain a strong score....

Starting credit the right way means paying on time, keeping balances low, avoiding too many applications, and monitoring your credit report. Avoiding these common mistakes helps you build a strong credit score faster and saves money on interest and fees....

Freezing your credit does not affect your credit score because it doesn’t change your credit report or history. It only blocks access to your file to prevent new accounts from being opened without your permission....

Credit freezes and credit locks both block access to your credit to prevent fraud. A freeze is free and legally protected, while a lock is a paid service offering easier controls and extra features like monitoring and alerts....

Building credit from scratch starts with a secured card or authorized user status, using small amounts, paying on time, and keeping balances low. With patience and consistent habits, you can build a strong credit history and open the door to better financial opportunities....

This planner-based approach helps you map a clear path out of debt by organizing balances, choosing a payoff strategy, setting rules, and tracking progress. With consistency and a simple plan, you can regain control of your money and move steadily toward a debt-free future....

Adults returning to school can qualify for many grants, including federal, state, school, and career-specific programs. By completing the FAFSA and applying widely, you can reduce tuition costs and make continuing your education far more affordable without taking on unnecessary debt....

You can build a simple, effective debt-free plan in 30 minutes by listing debts, choosing a payoff strategy, finding extra money, setting rules to avoid new debt, and following a clear action plan. Clarity and consistency turn progress into lasting financial freedom....

Free tools like budget, expense, debt, savings, and investment calculators help you understand your money, set clear goals, reduce debt faster, and grow wealth. Used together and consistently, they create a simple system for smarter, stress-free financial decisions....

Financial tools like budget, debt, and investment calculators help you understand your money, set clear goals, and plan smarter. By using them regularly and with accurate data, you can make better decisions, avoid mistakes, and build long-term financial stability....

Deciding between paying off debt or investing depends on interest rates, stability, and goals. Eliminate high-interest debt first, build an emergency fund, and consider a balanced approach that combines investing with steady debt reduction to grow wealth and reduce financial stress....

The right side hustle can meaningfully grow your savings if it has low startup costs, flexible hours, and real profit potential. Focus on skills or services that pay well, avoid high-risk schemes, and save the extra income intentionally....

Build credit from scratch by starting with a secured or beginner card, using it lightly, paying in full and on time, and keeping balances low. With consistency and patience, you can establish a solid credit history within a year....

A budget calculator helps you track income and expenses, spot overspending, set realistic goals, and plan smarter. By updating it regularly, you gain control over your money, reduce stress, and build better habits for saving, spending, and paying off debt....

If your life, income, or health needs have changed, or your plan causes high out-of-pocket costs or limits access to care, it may be time to upgrade. Reviewing options yearly helps ensure your insurance still fits your needs and budget....

This guide explains what new drivers must check in their first car insurance policy, including liability limits, collision and comprehensive coverage, deductibles, uninsured motorist protection, medical coverage, discounts, and exclusions, helping you choose proper protection without overpaying....

Freelancers and side-hustlers must choose their own health insurance, balancing cost, coverage, and risk. Options include marketplace plans, private insurance, or joining a partner’s plan, with subsidies and tax deductions helping reduce the overall cost....

Freezing your credit takes about ten minutes, costs nothing, and blocks criminals from opening accounts in your name. This step-by-step guide explains exactly how to freeze your credit with all bureaus and how to lift it temporarily when you need new credit....

Freezing your credit blocks criminals from opening accounts in your name, costs nothing, and takes only minutes to set up. Learn why it is one of the strongest protections against identity theft and how to easily freeze and unfreeze your credit when needed....

Learn which federal, state, school, and private grants you may qualify for as a low-income student, how financial need can work in your favor, and how to combine multiple grants to significantly reduce or eliminate the cost of your education....

Discover how to find hidden grants that don’t require repayment by targeting local and niche opportunities, using smart search strategies, following relevant organizations, and building a simple system to apply consistently and improve your chances of getting funded....

If your financial aid offer isn’t enough, review it carefully, appeal the decision, search for more scholarships, cut costs, consider work options, and use loans wisely. Sometimes choosing a more affordable school can lead to a stronger financial future....

The right amount of life insurance depends on your income, debts, family needs, and goals. By calculating expenses, replacing income, and subtracting existing assets, you can choose coverage that truly protects your family’s financial future....

Hidden fees and surprises in car insurance can be avoided by understanding your coverage, removing unnecessary add-ons, choosing the right deductible, checking billing methods, and reviewing your policy regularly. Smart comparison and asking for discounts help keep costs predictable and fair....

Term life insurance offers affordable, temporary coverage for specific needs, while whole life provides lifelong protection with a cash value component. The right choice depends on your budget, goals, and whether you want simple protection or long-term financial planning benefits....

Health insurance costs go far beyond premiums. Deductibles, copays, coinsurance, out-of-network charges, and uncovered services can lead to big bills. Understanding these hidden costs helps you choose better coverage, avoid surprises, and protect your finances from unexpected medical expenses....

Many low-income filers miss refunds due to common mistakes like not filing, choosing the wrong status, or skipping valuable credits. By checking eligibility, reporting all income, and using free tax help, taxpayers can avoid errors and maximize their refunds....

The Earned Income Tax Credit (EITC) helps low- and moderate-income workers get a larger tax refund, even if they owe little or no tax. By meeting income and filing requirements and submitting a return, eligible taxpayers can claim this valuable credit....

Your financial success depends more on behavior than math. Emotions, habits, and beliefs shape how you save, spend, and invest. By understanding your mindset, avoiding emotional decisions, and building consistent habits, you can achieve more stable, long-term financial results....

The Child Tax Credit helps families reduce their tax bill and may increase their refund. By meeting age, income, and dependency requirements and filing a return correctly, eligible parents can claim this valuable credit for each qualifying child....

Stocks offer simplicity, liquidity, and easy diversification, while real estate provides potential cash flow and leverage but requires more time, capital, and effort. The best choice depends on your goals, risk tolerance, and how hands-on you want to be as an investor....

Investing doesn’t have to be complicated. Beginners can start with ETFs for diversification, stocks for growth, or robo-advisors for automation. The key is to start early, invest regularly, and focus on long-term growth rather than short-term market moves....

Tax credits reduce your tax bill dollar for dollar and can even increase your refund. By understanding refundable and nonrefundable credits and claiming those you qualify for, you can significantly lower what you owe or boost your return....

FinTech loans are changing how people borrow money. Discover how digital lending works, its advantages, hidden risks, and when online loans are a smart financial choice....

Choosing between fixed and variable rate loans affects your monthly payment and total cost. Learn the pros, cons, risks, and when each option makes sense for mortgages, car loans, and personal loans....

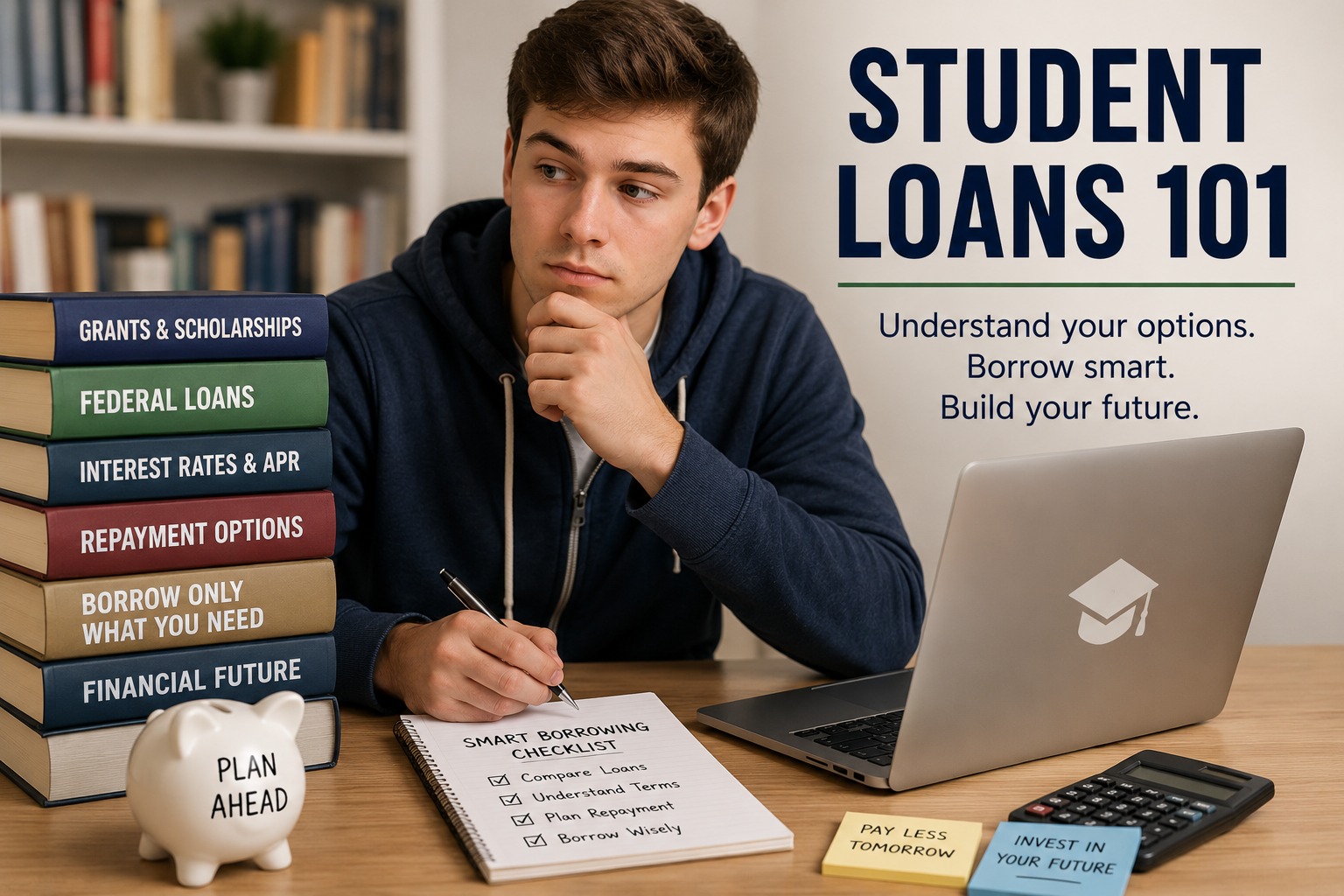

Student loans can make college possible, but smart borrowing is critical. Learn how to choose the right loans, borrow only what you need, control interest costs, and avoid long-term regret after graduation....

A practical guide to building a debt payoff plan by organizing debts, stopping new spending, choosing the right strategy, finding extra money, and staying consistent, showing how small, steady actions can lead to long-term financial freedom and lasting control over your money....

Raising your credit limit can improve your credit score by lowering utilization, but it also increases the risk of overspending. Learn when it makes sense to ask, when to wait, and how to use a higher limit responsibly....

A clear guide to which insurance policies are essential—health, auto, home or renters, life, and disability—and which ones are often a waste of money, helping readers focus on protecting themselves from major financial risks instead of minor, manageable losses....

The most common life insurance mistakes, including waiting too long to buy, choosing the wrong coverage, underestimating your needs, failing to update beneficiaries, and relying only on employer plans, helping readers avoid costly financial gaps in protection....

Health insurance costs go beyond the monthly premium. Learn how deductibles, co-pays, coinsurance, and out-of-pocket limits work together, how they affect your total healthcare costs, and how to choose the right health plan for your budget and medical needs....

Single parents can save thousands on taxes by using Head of Household status, the Child Tax Credit, Earned Income Tax Credit, and childcare credits. Learn the best tax tips to reduce your tax bill, boost your refund, and stretch your budget further....

Getting a loan with bad or no credit is possible, but it often comes with higher costs. Learn the best loan options, how to improve approval chances, avoid predatory lenders, and use borrowing strategically to rebuild your credit profile....

Small business loans can help entrepreneurs start, grow, or stabilize their companies, but choosing the wrong financing can hurt cash flow. Learn the main loan types, costs, risks, and how to borrow strategically for long-term success....

Most loans cost far more than their interest rate suggests. Hidden fees, penalties, variable rates, and long terms quietly increase what you repay. Understanding APR, total costs, and fine print helps you avoid expensive borrowing mistakes....

Identity theft and credit fraud can cause serious financial damage, but strong passwords, careful data habits, regular account monitoring, and tools like credit freezes can greatly reduce your risk and limit the impact of fraud....

Homeownership costs far more than just the mortgage. Property taxes, insurance, maintenance, utilities, and unexpected repairs add up quickly, making it essential to budget for the true, long-term cost of owning a home....

Retirement planning depends on estimating your future expenses, accounting for inflation and healthcare, and starting early. The sooner you save and invest consistently, the more flexible and secure your retirement options become....

Big life changes like marriage, kids, and buying a home require a new budget, strong emergency savings, planning for one-time costs, and smart automation to stay in control, avoid debt, and protect long-term financial stability....

Online checking and savings accounts are becoming smarter, faster, and more automated, with better security, higher yields, and built-in financial tools that help users manage money, save effortlessly, and gain more control over their financial lives....

An emergency fund should cover 3–6 months of essential expenses, be kept in safe, accessible accounts like high-yield savings, built through automation and windfalls, and used only for real emergencies to provide financial security and peace of mind....

Rent, utilities, and health insurance usually aren’t directly deductible, but they can affect your taxes through credits, deductions, and eligibility rules. Understanding their impact helps you plan smarter and potentially keep more money....

Low-income workers can increase their tax refunds by claiming credits like EITC, Child Tax Credit, and others. Filing a return and using available tools ensures you don’t miss money you deserve....

A smart debt payoff planner helps you organize every balance, choose the best payoff strategy, build a realistic budget, and track progress. With consistent payments and a clear roadmap, you can stay motivated, avoid setbacks, and confidently reach a zero-balance future....

A smart budget calculator simplifies money management by organizing expenses, revealing spending patterns, and letting you test financial scenarios. It helps you save more, reduce debt, and make confident financial decisions with a clear, easy-to-follow plan....

Grants are free money for college, and many students miss out. Complete the FAFSA early, explore federal, state, school, and private grant options, stay organized with required documents, and reapply each year to maximize financial aid and reduce college costs....

You can secure the best auto loan by knowing your budget, checking your credit, getting preapproved, comparing rates, and avoiding dealer upsells. Focus on total cost—not monthly payments—to avoid overpriced add-ons and drive away with a smarter deal....

A personal loan can be a helpful tool when used wisely. Understand interest rates, fees, and qualification requirements, compare multiple lenders, and choose a loan that fits your budget to avoid unnecessary debt and borrow confidently....

You can pay off your loan faster by making extra payments, switching to biweekly installments, refinancing to shorter terms, and cutting small expenses. These simple habits reduce your principal quicker, lower interest costs, and help you become debt-free sooner....

Lower your car insurance by comparing quotes, raising deductibles, bundling policies, asking for discounts, improving credit, reducing mileage, removing unnecessary coverage, driving safely, using tracking devices, and paying upfront. Small steps can lead to big savings quickly....

Life Insurance protects your loved ones financially. Get term insurance for affordable coverage during key years and consider whole life for lifelong protection. Buy earlier for lower rates, and choose coverage based on income, debts, and your family’s future needs....

Choose health insurance by focusing on your needs, comparing total yearly costs, checking networks and prescriptions, and using online tools. Understanding key terms and benefits makes the process easier and helps you pick a plan that fits your budget and lifestyle....

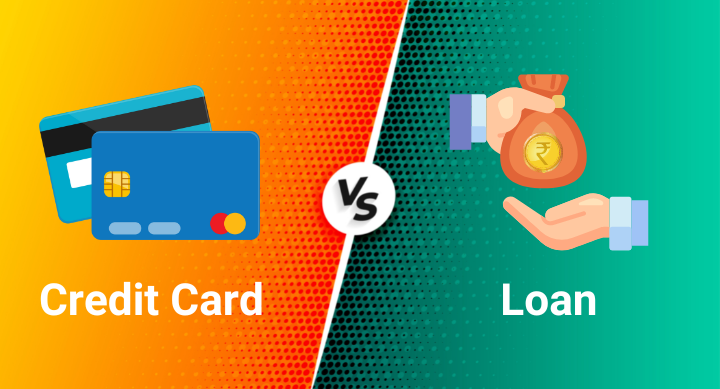

Use a credit card for smaller purchases you can pay off quickly, especially if you’ll earn rewards. Choose a personal loan for larger expenses or longer repayment needs, often with lower interest and predictable monthly payments. ...

Regularly reviewing your credit report helps protect your financial health. Check personal details, account accuracy, inquiries, and negative marks. If you find errors, dispute them with the credit bureaus and creditors using documentation. Correcting mistakes can improve your score and prevent fraud....

Kids build strong money habits long before college. Teaching saving, budgeting, earning, credit basics, and everyday financial decisions early helps them grow into confident, responsible adults who understand money, avoid costly mistakes, and make smarter choices throughout life....

Couples can avoid money conflicts by talking openly, choosing a shared financial system, creating a joint budget, and setting personal “fun money.” Regular check-ins and clear long-term goals help build trust, reduce stress, and make financial planning a true team effort. ...

An emergency fund protects you from unexpected expenses. Aim to save three to six months of essential costs, starting small and building over time. Keep the money in a high-yield savings or money market account for safety, liquidity, and easy access....

Understanding deductions, credits, and simple tax planning helps you keep more of your money. By tracking expenses, adjusting withholding, using free filing tools, and claiming key credits, you can reduce your tax bill and boost your refund with ease....

If you earn under $50,000, you can file taxes easily using free IRS tools or VITA. Gather income forms, choose the right filing status, claim key credits like EITC and CTC, and file electronically with direct deposit for the fastest refund....

Free tax help is widely available through IRS Free File, VITA, TCE, and AARP Tax-Aide. These programs offer free online tools or in-person assistance for eligible taxpayers, ensuring accurate, reliable filing without paying a preparer....

Maximize financial aid by filing the FAFSA early, checking for errors, exploring state and school grants, applying for scholarships year-round, appealing for changed finances, considering work-study, and comparing all award letters to find the best true cost....

The right car insurance balances legal requirements, personal risk, and budget. Compare quotes, choose proper coverage limits, select a realistic deductible, and consider valuable add-ons. Reevaluate yearly to ensure your policy still fits your needs and protects you financially....

Debt consolidation simplifies payments and lowers interest without hurting your credit, while debt settlement reduces what you owe but damages your score and may trigger taxes. Choosing the right option depends on your income, credit, and financial situation....

Choose bank accounts that work for you—low fees, great apps, strong security, fast transfers, and high-yield savings. The right checking and savings setup keeps your money safer, grows your balance faster, and makes everyday banking effortless....

Many low- and moderate-income taxpayers miss valuable credits like the Earned Income Tax Credit, Child Tax Credit, Saver’s Credit, and education credits. These can reduce your tax bill or increase your refund, even if you owe nothing. Don’t leave money unclaimed....

A budget you’ll stick to starts with tracking your spending, choosing a realistic method, automating savings, allowing fun money, and reviewing monthly. Focus on progress—not perfection—to build sustainable habits and long-term financial control....

You can file your taxes for free using IRS Free File, select free software tiers, fillable forms, or community programs like VITA and TCE. Each option avoids hidden fees and works best depending on your income, return complexity, and comfort level....

This guide explains when refinancing student loans makes financial sense and when it can be risky. It compares federal and private loan options, highlights key protections, and helps borrowers decide the safest, smartest repayment path. ...

A practical guide to choosing a credit card that fits your lifestyle, spending habits, and financial goals. Learn how to compare rewards, fees, interest rates, and benefits so your card truly works for you. ...